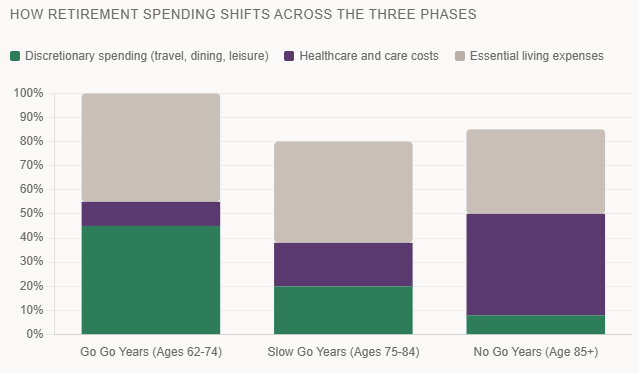

The Go Go Years, the Slow Go Years, and the No Go Years

Most retirement projections make a quiet assumption that turns out to be wrong: that your expenses will be roughly the same every year. Run the numbers at 65, divide by 30, and you have your annual budget. It is a tidy model. It is also a significant oversimplification of how retirement actually unfolds.

The reality is that retirees tend to spend in a pattern that looks more like a wave than a flat line. Early in retirement, spending is often at its highest. People travel, pursue hobbies, help grandchildren, and live actively. Over time, that activity naturally slows. And in the final years, discretionary spending drops sharply while healthcare costs often rise to take its place.

Financial planners have long used three plain-spoken terms to describe this arc: the Go Go Years, the Slow Go Years, and the No Go Years. Understanding which phase you are in, and planning financially for all three, is one of the most important things a retiree can do.

The Go Go Years

Roughly ages 62 to 74

This is the season most people picture when they imagine retirement. You are healthy, energetic, and finally free from the structure of work. The bucket list comes off the shelf. Cruises get booked. Grandchildren get visited. Golf memberships get used. This is the phase where retirement living actually costs the most.

Research consistently shows that newly retired households spend at rates close to, and sometimes exceeding, their pre-retirement spending. The combination of newfound time and the desire to enjoy it fully is a powerful force. Many retirees also use these years to downsize their home, renovate, help adult children or fund grandchildren's education.

From a planning standpoint, this phase requires the most liquidity and flexibility. It is also the phase where sequence of returns risk is greatest. A major market downturn in your first few years of retirement, combined with high withdrawal rates, can permanently impair a portfolio in ways that are very difficult to recover from.

The Slow Go Years

Roughly ages 75 to 84

The pace shifts. Not because the desire to live fully goes away, but because energy and mobility naturally begin to change. Long-haul international trips may give way to regional travel or extended stays with family. The golf game continues, but perhaps three rounds a week becomes one. Life gets quieter, and in many ways, more deliberate.

Spending on travel and entertainment typically declines meaningfully in this phase. Studies from the Employee Benefit Research Institute found that household spending drops by roughly 25 to 30 percent between the early and mid-retirement years in real terms. That is a significant shift that most retirement projections fail to model.

At the same time, new costs begin to appear. Routine health maintenance becomes more involved. Prescription costs may rise. Some retirees begin paying for home services they once handled themselves, like yard work, home repairs or housekeeping. The spending curve does not fall off a cliff. It reconfigures.

The biggest planning mistake I see in this phase is not accounting for the spending decline. People are often sitting on more than they need mid-retirement because they planned as if the Go Go spending would last forever.

The No Go Years

Roughly age 85 and beyond

By this phase, the world has largely contracted to a smaller, more familiar radius. Extended travel is rarely on the table. Dining out becomes occasional rather than regular. The discretionary budget that defined the Go Go Years is a fraction of what it once was.

What rises sharply in its place is the cost of care. Whether that means in-home assistance, assisted living, memory care or skilled nursing, the financial demands of late-life healthcare can be substantial. This is the phase that long-term care insurance, health savings accounts and Medicaid planning are designed to address.

It is also the phase where estate planning matters most. Required minimum distributions are in full swing. The question of how assets will transfer to heirs becomes pressing. And for many families, the practical and emotional decisions around end-of-life care begin to require real coordination.

A well-structured retirement income plan anticipates this phase from the very beginning. The assets that were not needed in the Slow Go Years can be positioned to fund care costs and protect a spouse or heirs from financial hardship.

What this means for how you plan

The three-phase model changes how you should think about almost every retirement planning decision. It affects how you structure your income, which accounts you draw from first, how you size your emergency reserves and when you make major spending commitments.

A flat "I need $X per year" retirement budget misses the fact that you will probably need more than that in your 60s and early 70s, somewhat less in your late 70s and early 80s, and then potentially much more again in your late 80s and beyond, driven almost entirely by healthcare. Planning for the average of those three phases means you are underfunded in two of them.

The better approach is a phased income plan that explicitly models all three stages. That means identifying which assets will fund discretionary spending in the Go Go Years, building a bridge to cover the transition into the Slow Go Years, and ensuring that a dedicated strategy exists for the healthcare and care costs of the No Go Years.

This kind of planning is not morbid. It is liberating. Retirees who have modeled all three phases tend to spend more freely in the early years, because they know their plan accounts for what comes later. The ones who have not tend to underspend out of anxiety, or overspend out of optimism, and get caught off guard either way.