What to Do With Your 401(k) When You Retire or Change Jobs

Leaving a job is one of the most financially consequential moments in a person's life, whether that departure is a retirement you have planned for decades or a career change you made last month. And one of the first decisions you will face is one that most people are completely unprepared for: what do you do with the 401(k) you are leaving behind?

The answer matters more than most people realize. Make the wrong move and you could trigger a tax bill you were not expecting, permanently lose years of compound growth, or lock yourself into investment options that no longer serve you. Make the right move and you preserve every dollar you have worked to save, gain flexibility you did not have before, and set yourself up for a more tax-efficient retirement.

The good news is that you have time to think it through. When you leave a job, your 401(k) does not disappear. It stays right where it is until you decide what to do with it. But the clock does eventually matter, so here is a clear-eyed look at your four options.

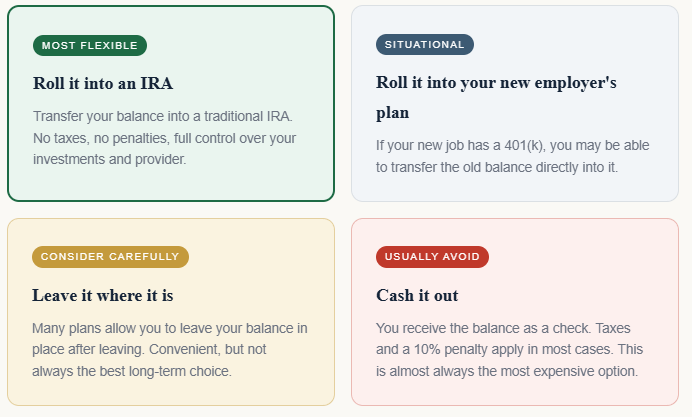

Option 1: Roll it into an IRA

For most people in most situations, rolling your old 401(k) into a traditional IRA is the smartest move. Here is why.

When done correctly as a direct rollover, the transfer is completely tax-free. The money moves from your old plan directly to your new IRA without ever touching your hands, which means no withholding, no tax event, no penalties. Every dollar continues to grow tax-deferred exactly as it did before.

The bigger advantage is what happens after the rollover. Inside a 401(k), you are limited to the investment options your employer chose, which typically means a menu of 20 to 30 mutual funds. Inside an IRA, you can invest in virtually anything: individual stocks, bonds, ETFs, mutual funds, REITs, and more. You also get to choose your own custodian, which means you can work with a financial advisor of your choosing rather than being tied to a plan administrator.

An IRA also gives you more flexibility around Roth conversions, beneficiary designations, and estate planning, which become increasingly important as you approach and enter retirement.

Option 2: Roll it into your new employer's plan

If you are changing jobs rather than retiring, and your new employer offers a 401(k), you may have the option to transfer your old balance directly into the new plan. This can make sense in certain situations.

The primary advantage is simplicity. Everything lives in one place, which makes it easier to manage. Some employer plans also offer institutional-class mutual funds with lower expense ratios than what you would find in a retail IRA, which can meaningfully impact long-term returns.

There is one specific scenario where rolling into a new employer plan is worth serious consideration: if you plan to keep working past age 73. Under current tax law, required minimum distributions from a 401(k) can be delayed if you are still working for that employer. That option is not available with an IRA, where RMDs begin at 73 regardless of your employment status.

The downside is that your investment options are again limited to whatever the new plan offers. And not all plans accept incoming rollovers, so you will need to check before assuming this option is available to you.

Option 3: Leave it where it is

You are generally allowed to leave your 401(k) with your former employer's plan indefinitely, provided your balance is above a certain threshold. If your vested balance is above $7,000, your former employer cannot force you out of the plan.

For a short-term transition, this can be a perfectly reasonable holding pattern. You are not making any irreversible decisions, your money continues to grow, and you buy yourself time to evaluate your options carefully.

Over the long term, though, leaving old 401(k)s scattered across former employers creates real problems. Accounts get forgotten. Investment allocations drift without attention. Beneficiary designations go stale. And consolidating multiple old accounts later is more work than simply rolling them over at the time of departure.

If you have changed jobs several times over your career, this is also a good moment to track down any accounts you may have left behind. A CFP or financial advisor can help you locate and consolidate old accounts into a single IRA, which simplifies management considerably.

Option 4: Cash it out

This is the option most financial advisors will tell you to avoid, and for good reason.

When you take a cash distribution from a 401(k), the full amount is added to your taxable income for the year. If you are under age 59½, a 10% early withdrawal penalty applies on top of that. Depending on your tax bracket, you could lose 30% or more of the balance before it ever reaches your bank account.

The more painful cost is the one you cannot see on your tax return: the permanently lost compound growth. A $50,000 distribution at age 45 does not cost you $50,000. It costs you what that $50,000 would have become by the time you retired, which at a 7% average annual return over 20 years is closer to $193,000.

"The decision you make with your 401(k) at a job transition is one of the few financial moves in life that is very hard to undo. It deserves more than 10 minutes of thought."

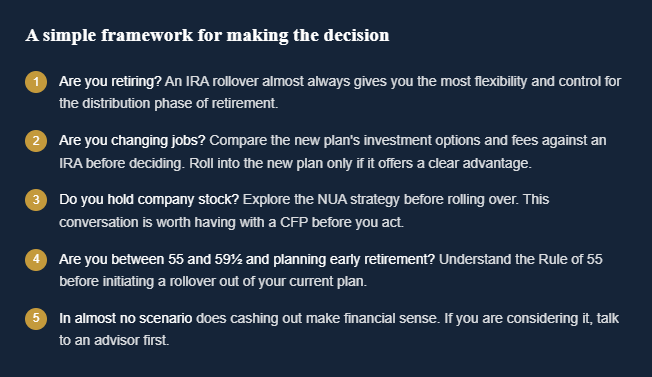

Special situations worth knowing about

A few scenarios that do not always make it into the standard rollover conversation:

The Rule of 55. If you leave your job in or after the year you turn 55, you can take distributions from that employer's 401(k) without the 10% early withdrawal penalty. This does not apply to IRAs and does not apply to 401(k)s from previous employers. If early retirement is your plan, this rule could influence whether you roll over immediately or leave the funds in place for a period.

Net unrealized appreciation. If your 401(k) holds company stock that has appreciated significantly, a specialized strategy called net unrealized appreciation (NUA) may allow you to pay long-term capital gains rates on that appreciation rather than ordinary income rates. This can result in significant tax savings for the right person in the right situation. It is one of the more overlooked planning opportunities in rollover conversations.

Roth 401(k) funds. If your employer offered a Roth 401(k) and you contributed to it, those funds should be rolled into a Roth IRA, not a traditional IRA. Keeping the Roth character of those dollars intact is important for preserving their tax-free growth and avoiding future required minimum distributions.

A job transition, whether into retirement or a new role, is one of the busiest and most emotionally charged periods of anyone's financial life. The 401(k) decision often gets made quickly, without full information, during a time when attention is already stretched thin. Taking even a few days to understand your options can make a meaningful difference in where you end up.

A job transition, whether into retirement or a new role, is one of the busiest and most emotionally charged periods of anyone's financial life. The 401(k) decision often gets made quickly, without full information, during a time when attention is already stretched thin. Taking even a few days to understand your options can make a meaningful difference in where you end up.